Naked calls are an options strategy used to generate income by collecting premium, allowing you to generate income when you expect the stock price to stay below a certain level. However, naked calls also carry significant risk, including the potential for unlimited losses. It’s incredibly important for beginners to understand the strategy thoroughly before using it.

What Is a Naked Call?

A naked call is created by selling a call option without owning the underlying stock. When you sell a call, you’re agreeing to sell the stock at the strike price if the option is exercised by the buyer. In return, you receive a payment called premium, which is your income for taking this obligation.

The term “naked” means you don’t own the stock you’re promising to sell. This is different from a covered call, where you already hold the shares and can deliver them if the option is exercised. Because you don’t own the stock, you face significantly more risk. If the stock price rises sharply above the strike price, you’d need to buy shares at the higher market price to sell them at the lower strike price.

Key Terms

- Premium: The payment you receive for selling the call option.

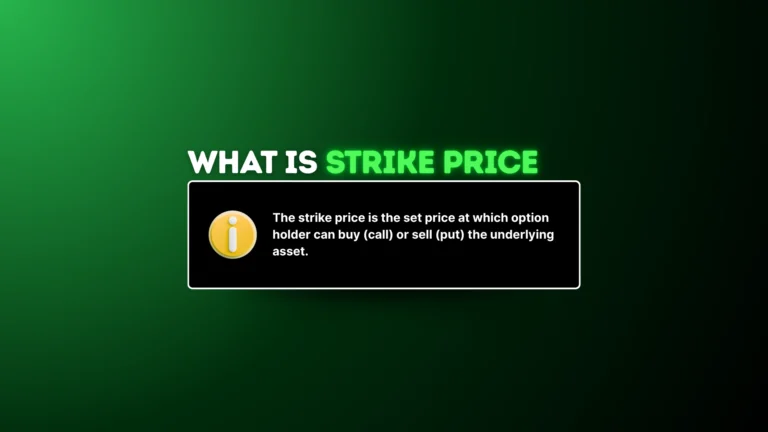

- Strike Price: The price at which you agree to sell the stock if the buyer exercises the option. For a $130 strike call, you must sell 100 shares at $130 each if the buyer demands it.

- Expiration Date: The deadline for the buyer to exercise the option. After this date, the option is either exercised or becomes worthless.

The Process of Selling a Naked Call

When you sell a naked call, you’re giving the buyer of the call the right to purchase 100 shares of a stock from you at a specific price. In exchange, you receive a payment which you get to keep in full if the stock remains below the strike price at expiration.

Here’s how it works:

- Choose a Stock and Option: You pick a stock you think will stay flat or drop in price before the option expires. For example, you might choose Tesla (TSLA) and sell a call option with a $300 strike price, expiring in 30 days, for a $2 premium. This means you collect $200 per contract (100 shares x $2).

- Sell the Call Option: Sell the call and collect the premium. Since you don’t own the underlying stock, this is a naked call. Your broker will require you to have a margin account and sufficient capital to cover potential losses.

- Wait for Expiration or Manage the Trade: Over the next 30 days, you hope Tesla’s stock price stays below $300. If the does, the option becomes less valuable each day due to time decay (a concept called theta). You may then choose to hold till expiration, or close the option early by buying it back.

Risks and Rewards

Selling naked calls can generate income but carry similar risk to shorting the underlying stock. You collect a premium for agreeing to sell shares at a set strike price, but if the stock surges, you could face massive losses.

The strategy has its benefits. You earn immediate income from the premium, secured if you hold until expiration. It’s a neutral-to-bearish strategy that profits if the stock falls, stays flat, or rises slightly. Most importantly, it ties up far less capital than selling a covered call which would require owning at least 100 shares of the stock.

Risks

- Limited Profit: Your max gain is capped at the premium received.

- Unlimited Losses: If the stock rises dramatically in price, you could be forced to buy the stock at a significantly higher price than where you initially sold it.

- Volatility Risk: Rising volatility can increase the price of the option, increases losses even if the stock price remains stable.

Rewards

- Regular Income: Earn steady income in the form of option premium.

- Low Capital Requirement: Unlike a covered call, you’re not required to hold shares of the underlying stock. The capital requirement will be far lower for a naked call.

- Time Decay: The premium is yours if the stock stays below the strike since the options value fades over time (Theta).

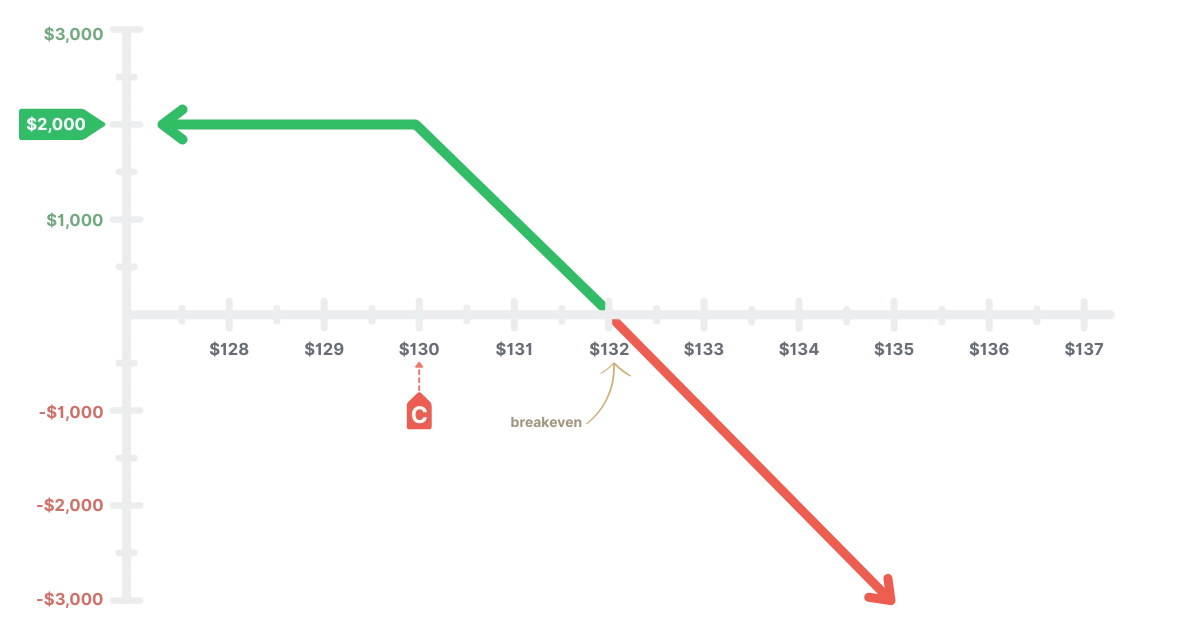

Example 1: Naked Calls on NVIDIA

Let’s assume you have a $50,000 trading account and sell 10 NVDA calls with a $130 strike price, expiring in 30 days. Each contract is sold for a $2 premium, so you collect $2 x 100 shares x 10 contract = $2,000 upfront. This premium is your max profit if the options expire worthless (i.e., NVDA stays below $130 at expiration). As the seller of the calls, you’re obligated to sell 1,000 shares (100 shares per contract x 10 contracts) at $130 a share if the buyer exercises their calls.

At expiration, let’s assume NVDA’s stock price is at $125, below your $130 strike. The options you sold expire worthless because no buyer would exercise a call to buy shares at $130 when they can buy them for $125 in the market. You keep the full $2,000 premium as profit, and the options expire worthless.

Profit Calculation

- Premium Collected: $2,000

- Cost to close: $0 (options expire worthless)

- Net profit: $2,000

| Max Profit | $2,000 | The premium received ($2 x 100 shares x 10 contracts) is your max profit. This is achieved if NVDA closes below $130 at expiration and all options expire worthless. |

| Max Loss | Unlimited | Losses continue to grow as NVDA’s price rises above $130. For example, at $140, you lose $10 per share x 1,000 shares – $2,000 premium = $8,000. If NVDA hits $200, the loss could grow to $68,000, limited only by how the stock rises. |

| Breakeven | $132 | The stock price at which your profit is zero. The strike price ($130) + premium ($2) = $132. |

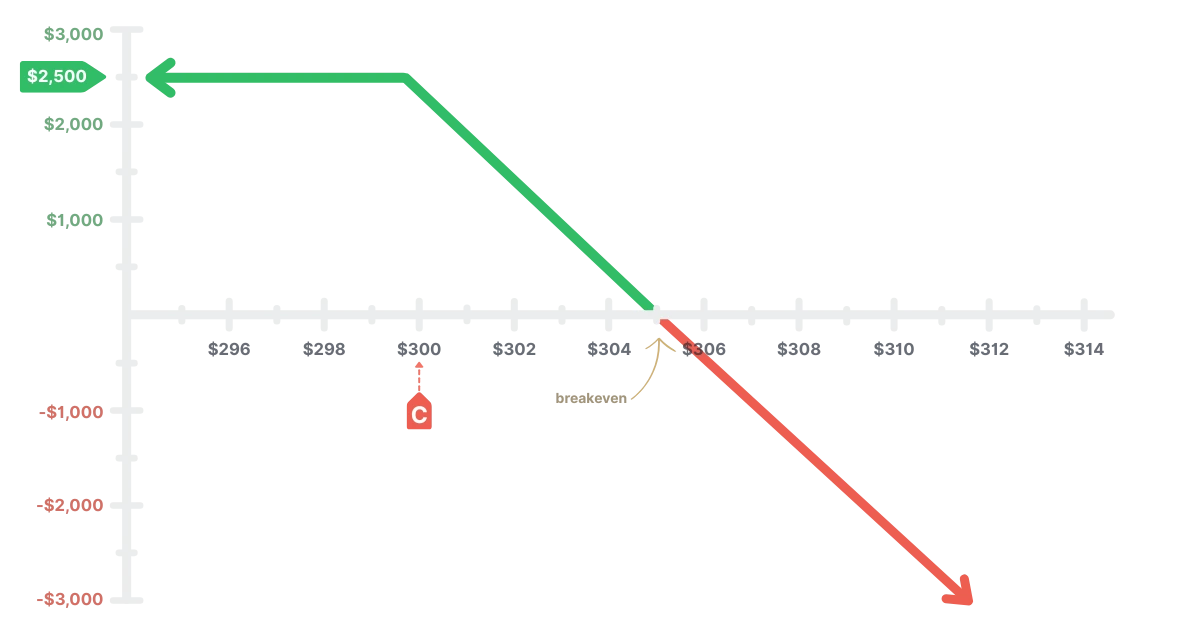

Example 2: Naked Call on Tesla

In this next example, let’s say you sell 5 TSLA call options with a $300 strike price, expiring in 30 days. Each contract is sold for a $5 premium, so you collect $5 x 100 shares x 5 contracts = $2,500 in total. As the seller of the calls, you’re obligated to sell 500 shares (100 shares per contract x 5 contracts) at $300 per share if the buyer exercises.

At expiration, let’s assume TSLA’s stock price rockets to $320, well above your $300 strike. The options are in-the-money (ITM), and the buyer exercises all 5 contracts. You’re obligated to sell 500 shares at $300 per share, but since you don’t own the shares, your broker assigned you a short position of -500 shares. With TSLA at $320, you buy back the stock to cover the short at the current market price. You incur a loss of -$7,500 in total.

Profit Calculation

- Premium collect: $2,500

- Cost to close: $20 per contract ($320 – $300 x 5 contracts = $10,000)

- Net loss after premium: $10,000 – $2,500 = -$7,500

| Max Profit | $2,500 | The premium received ($5 x 100 shares x 5 contracts) is your max profit, only achieved if TSLA closes below $300 at expiration and the options expire worthless. |

| Max Loss | Unlimited | Losses grow as TSLA’s price rises above $300. For example, at $320, you lose $20 per share x 500 shares – $2,500 premium = $7,500. If TSLA hits $400, the loss could be $47,500, limited only by how high the stock climbs. |

| Breakeven | $305 | The stock price at which your profit is zero. The strike price ($300) + premium ($5) = $305. |

Greek Exposure in Naked Calls

When you sell a naked call, you’re taking on a high level of risk since there is no limit to how high the stock can rise. To navigate this strategy, you need to understand the Greeks. These metrics will show you how your options value changes with factors like stock price, time, volatility, and interest rates.

These Greeks (Delta, Gamma, Theta, Vega, and Rho) are like a dashboard for your trade, helping you better understand the risks and rewards.

Delta (Δ)

Delta tells you how much your call will change in value when the stock price moves by $1. As a call seller, your Delta is negative, meaning you profit from the stock price falling. Your goal is for the options price to go down, ideally to zero, so you keep the full premium you collected when selling the call. If the stock price rises, the call increases in price, which is bad for you because it increases your potential losses.

For example, imagine you sell a $130 call on NVDA for a $2 premium ($200 per contract, and the Delta is -0.30. If NVDA’s stock price rises from $125 to $126, the option would increase by $0.30 ($30 per contract). Meaning the call would move from $2 to $2.30, leaving you with an unrealized loss of $30.

Gamma (Γ)

Gamma measures how much Delta changes when the stock price moves by $1, and for a naked call, its negative. This means as the stock price rises, your Delta becomes more negative, making your position even more sensitive to further price increases.

For example, suppose the $130 NVDA call from earlier has a Delta of -0.50 and a Gamma of -0.05. If NVDA jumps $2 from $129 to $131, Gamma could push your Delta to -0.60 or more. This means another $1 move would cost $60 per contract instead of $50.

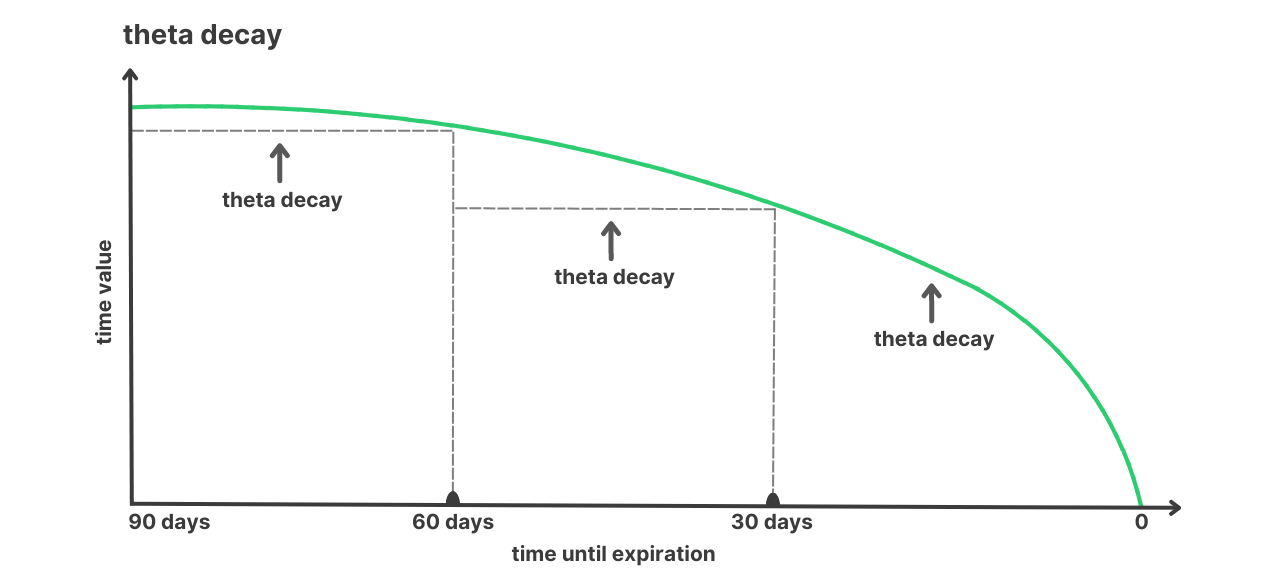

Theta (Θ)

Theta represents time decay, how much the options value drops each day as expiration gets closer. For a naked call, Theta is positive, which is great news for you as the seller. The option loses value daily, increasing your profit if the stock stays below the strike price. For example, if your $130 NVDA call has a Theta of +0.05, you gain $5 per contract for every day that passes (assuming the stock price doesn’t move).

This effect gets stronger closer to expiration, as the options time value erodes faster. Selling calls with 30 – 45 days till expiration can maximize this return. The decay curve below shows how Theta grows exponentially as the option nears expiration.

Vega (ν)

Vega measures how the options price reacts to a 1% change in implied volatility (IV). This being the markets expectation of future price swings. For a naked call, Vega is negative, meaning a rise in IV increases the value of option value, which hurts you as the seller. For example, if your $130 NVDA call has a Vega of -0.10 and IV jumps from 30% to 31%, the options price would rise by $10 per contract.

High IV makes options more expensive, which is why many option sellers target high-IV environments (e.g., before earnings) to collect larger premiums. The hope is that IV drops after the event, reducing the options value.

| Greek | Measures | Put Seller |

|---|---|---|

| Delta (Δ) | Stock price movement | (-) Benefits from stock price decreasing |

| Gamma (Γ) | Rate of change of delta | (-) Delta decreases as stock price falls and increases as stock price rises |

| Theta (Θ) | Time decay | (+) Benefits from time decay |

| Vega (ν) | Volatility changes | (-) Benefits from volatility decreasing |

Managing Your Naked Calls: Closing, Rolling, or Accepting Assignment

Selling naked calls can generate income, but the potential for unlimited losses means you need a plan to manage your position. As a beginner, you have three main options to handle a naked call before or at expiration: closing the position, rolling the option, or accepting assignment.

- Closing the Position: Closing a naked call means buying back the same call option you sold to exit the trade. This locks in your profit or loss and removes any further obligation to sell shares. You might choose to close if the stock price begins rising towards your strike price or if it’s dropped significantly.

- Rolling the Option: Rolling is simply closing the current naked call by buying it back and simultaneously selling a new call option with a later expiration date, a different strike price, or both. This extends your trade, allowing you to collect more premium or delay a potential assignment. You might roll if the stock price nears your strike (to avoid assignment) or if you believe the stock will stabilize or drop later.

- Accepting Assignment: Accepting assignment means fulfilling your end of the contract, selling shares at the strike price when the buyer chooses to exercise. This typically occurs at expiration when the stock price is above the strike (in-the-money). Since you don’t own the stock, you’d be holding a short stock position of -100 shares for every contract you sold.