An option premium is simply the price of an option contract. Think of it as the cost you pay as the buyer when purchasing a call or put option, or the amount you receive as the seller when you sell that option.

An option’s premium isn’t just some arbitrary price throw out by the market. It’s carefully structured, a blend of two distinct parts. Intrinsic value and extrinsic value. Think of it as a layered cake. The base layer is the solid stuff, the real meat of what the option’s worth right now. That’s the intrinsic value. The top layer, fluffier, more speculative, is the extrinsic value, often called time value.

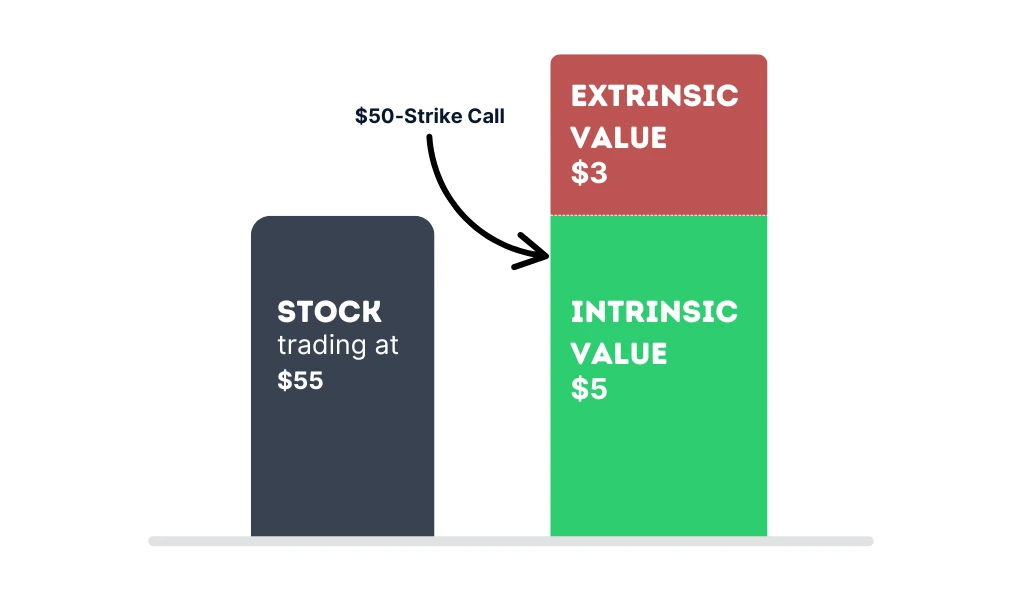

Intrinsic Value: What’s Already Yours

Intrinsic value is the actual, tangible worth built into an option. It’s what the option would be worth if you exercised it today, right now. For a call option, it’s calculated by taking the current price of the underlying stock and subtracting the strike price. For example, if a stock is trading at $120 and your call option has a strike price of $100, the intrinsic value is $20.

If that number is negative, it means the option is out-of-the-money and has no intrinsic value. Only in-the-money options have intrinsic value, otherwise it’s zero.

Put options work in the opposite direction. You take the strike price and subtract the stock’s current market value. So if the put’s strike is $150, and the stock’s trading at $140, that put has $10 of intrinsic value.

Intrinsic value is straightforward, rooted in simple math. You look at where the stock is now, compare it to the strike price, and that difference is your value. No what-ifs, just the real, in-the-money amount you’d get if you exercised the option right then.

Extrinsic Value: The Price of Possibility

Extrinsic value is trickier. More abstract. It’s the “what if” part of the options premium. The part that accounts for what could happen between now and expiration. Traders often call this time value, but that’s just one piece of it. Really, extrinsic value includes anything outside the intrinsic value. Time until expiration, volatility, upcoming news, anything that could shift the stocks trajectory.

Extrinsic Value = Option Premium – Intrinsic Value

If you’re holding a call that’s $20 in-the-money, but the market price is showing a $27 premium, that extra $7 is the extrinsic value. That extra $7 is the cost of that future uncertainty. It represents the added cost of time, volatility, and potential.

As expiration draws near, extrinsic value begins to erode. Slowly at first, then faster and faster. This is theta decay, and it’s relentless. And by the time we reach expiration, extrinsic value will always be zero and all you’re left with is intrinsic value.

In short, intrinsic value is what your option is worth now. Extrinsic value is what you’re paying for possibility. Combined, they make up the total premium and pricing of an option contract.

Factors Affecting Option Pricing

Option prices don’t exist in a vacuum. They’re living, moving things, influenced by a web of market forces. Some are obvious, while others less so. Together, they create the premium you see flashing on your screen. Understanding what pushes that number higher (or pulls it down) is essential if you’re serious about options.

1. Stock Price Relative to the Strike Price

At its core, an option’s value depends on how far in or out-of-the-money it is. When the stock price climbs above a calls strike price, or falls below a puts strike, the option gains intrinsic value. The deeper it goes, the more valuable it becomes.

This is the first thing traders look at. It’s also the most direct. A sudden price move in the underlying stock can instantly shift the premium, up or down.

2. Time until Expiration

Time equals opportunity. The more time an option has before expiration, the more chances the underlying has to move. That extra possibility costs money. That’s why longer-dated options come with higher premiums.

But time isn’t static. It erodes. And the closer an option gets to its expiration date, the less valuable that time becomes. This is time decay in action. It starts slow, then speeds up.

3. Volatility

Volatility is the wild card. It doesn’t care about direction, only movement. The more volatile a stock is, the more likely it is to swing in either direction. That makes options more expensive because with big swings, anything can happen.

The market anticipates this through implied volatility. This is a forward looking estimate of how much movement is expected in the stock. High implied volatility inflates premiums. Low implied volatility deflates them. It’s supply and demand driven, while also deeply phycological.

4. Interest Rates

When interest rates rise, the value of call options tends to increase, while the value of put options often decreases. Lowering rates flips that. It’s a subtle effect, but real.

Here’s why it happens.

Buying a stock outright requires capital. If interest rates are high, that capital comes with an opportunity cost since you could be earning more just by parking it in a money market fund or short-term bonds. Calls offer a workaround. Instead of tying up a large sum buying the stock, you can control it through a smaller premium. That makes calls more attractive in higher-rate environments, increasing demand, causing the premium to go up.

Now flip the scenario. When interest rates fall, cash becomes cheap. The cost of holding a stock outright drops, which reduces the comparative advantage of using calls. That softens call premiums. Meanwhile, puts become a bit more desirable, especially in uncertain or bearish markets, and their value can edge higher.

5. Dividends

Dividends can also impact pricing, especially for calls. When a company pays a dividend, the stock price usually dips by that amount. If you’re holding a call, that drop isn’t great news. To adjust for this, call premiums tend to be slightly lower when a dividend ex-date is approaching, accounting for the expected drop. Whereas puts might see a slight bump in price.

Option Greeks & Option Pricing

The price of an option isn’t just about where the stock is now. It’s about how that price reacts as the market shifts around it. And that’s exactly what the Option Greeks explain.

The Greeks show you how your option responds to time passing, price movement, and to changes in volatility. They break it down so you’re not left guessing why your option suddenly dropped or why it just spiked without warning.

Delta (Δ)

Delta measures how much the option’s price will move with a $1 change in the underlying asset. A delta of 0.60 means the option will gain or lose $0.60 for a $1 move in the stock.

- Calls have positive delta.

- Puts have negative delta.

The deeper an option is in-the-money, the closer the delta gets to 1 or -1. The further out-of-the-money an option goes, the closer its delta gets to zero.

Gamma (Γ)

Gamma shows how much delta will change when the underlying price moves. It reflects the curvature or acceleration of an option’s price movement.

High gamma means your delta is changing quickly, which can be both a threat and an opportunity. Near-the-money options with shorter expirations usually have the highest gamma.

Theta (Θ)

Theta is the enemy of all long option holders. It measures how much value an option loses each day as the expiration date approaches.

- Theta is negative for buyers.

- Theta is positive for sellers.

As expiration nears, theta decay accelerates. Holding options too long without a clear move can erode value quickly.

Vega (ν)

Vega measures how sensitive an options price is to changes in implied volatility. When implied volatility rises, option premiums go up. When it falls, they drop. This applies to both calls and puts.

It makes sense when you think about it. Volatility represents potential movement. The more move expected in the underlying stock, the more likely it is that the option could end up in-the-money. That extra possibility has value, and the market charges you for it.

Rho (ρ)

Rho tells you how much an options price changes with a 1% move in interest rates. It’s more noticeable in longer-term options.

- Call options rise when rates go up (positive Rho).

- Puts lose value when rates increase (negative Rho).

In low-rate environments, Rho matters less. But it does become more relevant in times of rising rates or for long-dated contracts.

| Greek | What It Measures | Impact on Options |

|---|---|---|

| Delta | Price movement sensitivity | Call delta is positive, put delta is negative |

| Gamma | Rate of change in delta | High near-the-money, increase risk and reward |

| Theta | Time decay | Hurts long position as time passes |

| Vega | Volatility impact | More volatility boosts both call and put premiums |

| Rho | Interest rate sensitivity | Calls gain with rising rates, puts lose value |