Cash secured puts can be a powerful strategy to generate income or buy stocks a discounted price. It’s a popular method for traders looking to manage risk while earning regular income in the form of option premium.

What Is a Cash-Secured Put?

A cash-secured put is created by selling a put option while setting aside enough cash to buy shares of the underlying stock at the strike price if assigned. When you sell a put, you’re agreeing to buy the stock at the strike price if the option is exercised by the buyer.

The “cash-secured” aspect is just to ensure you have the cash available in the account to buy the stock if assigned. If you didn’t have the cash available to buy the stock it would instead be called a “naked put.”

Key Terms

- Premium: The income you receive for selling the put.

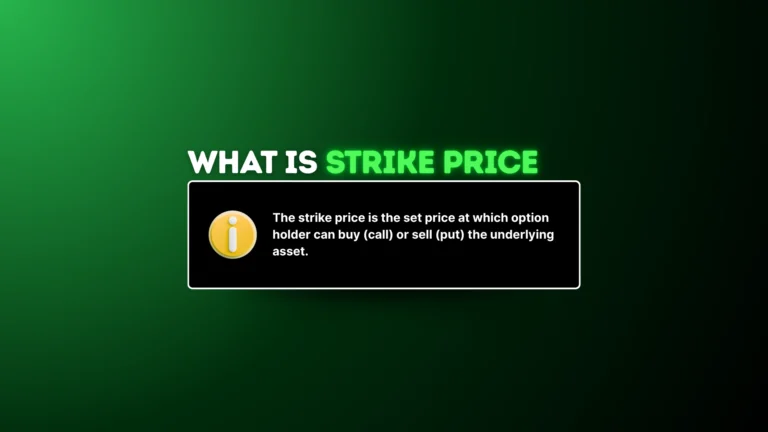

- Strike Price: The price at which you’ll buy the stock if assigned.

- Expiration Date: The date by which the option must be exercised or expires worthless.

How Does It Work?

The process is pretty straightforward, but let’s break out the trade one step at a time.

- Choose a Stock: Pick a stock you’d like to own or believe will remain stable or rise in price.

- Select the Strike Price: Determine the price at which you’d feel comfortable buying the stock. This becomes the strike price of the put option.

- Sell the Put: Sell the put and collect a premium upfront. This premium is also your max profit.

- Hold Sufficient Cash: Ensure your account holds enough cash to buy 100 shares of the stock at the strike price.

- Monitor the Position: Manage the position until expiration or close the trade early by buying back the put.

Let’s say you like AAPL, currently trading at $200 a share, but you’d prefer to buy it cheaper, say at $190. Instead of waiting, hoping the stock drops, you sell a put option with a strike price of $190 expiring in a month. You receive an immediate premium (income) of $2 per share ($200 total for a single contract).

Possible Outcomes:

- Stock stays above $190: The put expires worthless, and you keep the full $200 premium.

- Stock drops below $190: You’re forced to buy 100 shares at $190, spending the $19,000 set aside when placing the trade. Your net cost, after accounting for the premium, is actually $188 per share ($190 strike – $2 premium).

Risks and Rewards

Selling cash-secured puts carries risks similar to owning the stock outright. When you sell a put you’re agreeing to buy the stock at the strike price if it drops – so a big price drop could leave you holding shares that have lost a significant amount of value. If instead the stock price skyrockets, your gains are capped at the premium you pocketed, missing out on the full upside of simply buy the stock.

On the flip side, the strategy certainly has it’s perks. You get immediate income from the premium, guaranteed if you hold till expiration. It’s also a neutral-to-bullish play that pays off if the stock goes up, stays flat, or even falls a bit. Best of all, if you’re a fan of the stock, you might end up buying shares at a better price.

Risks:

- Limited Upside: The max profit is capped at the premium received.

- Significant Loss Potential: If the stock drops dramatically in price you could end up owning shares at a substantial loss.

- Opportunity Cost: The cash set aside can’t be used for other investments until the expiration or until put is closed.

Rewards:

- Regular Income: Earn regular income in the form of premium.

- Buying Discounted Stocks: Potentially buy stock at prices lower than the current market price.

- Downside Buffer: The premium received provides a cushion against losses, lowering your effective cost basis (purchase price).

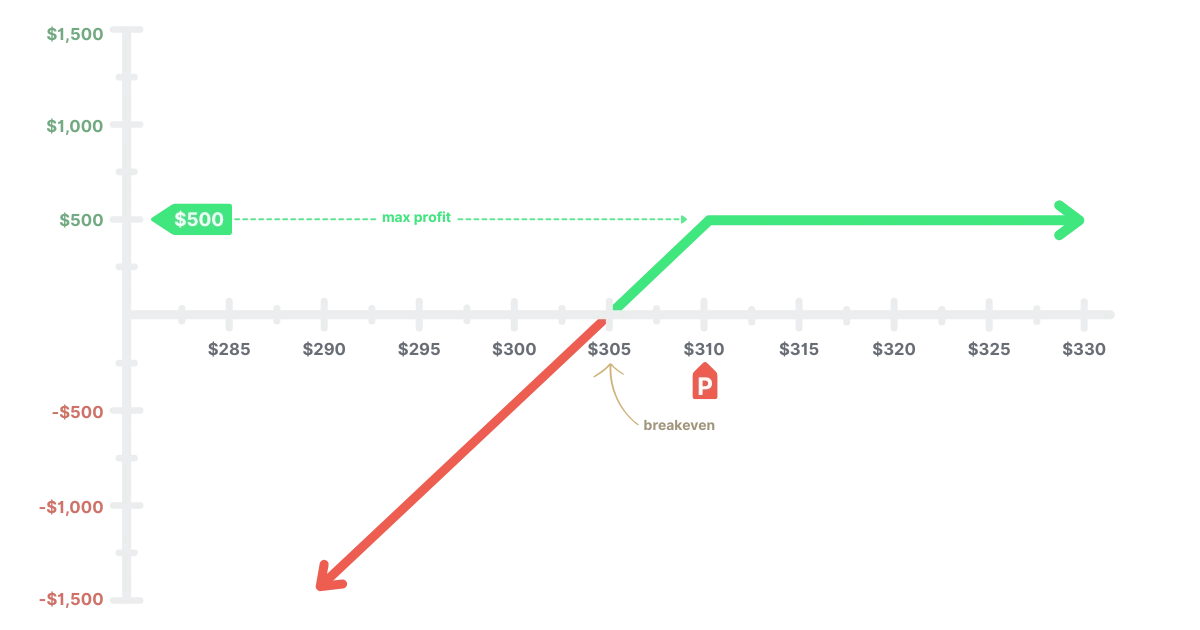

Example 1: Cash-Secured Put on Microsoft

For this example, let’s look at Microsoft (MSFT), currently trading at $320. You’re willing to own the stock at a slightly lower price and decide to sell a cash-secured put:

- Selling the Put: You sell a put with a $310 strike price and collect a $5 premium per share ($500 total for one contract).

- Cash Requirement: To sell this put, you must reserve $31,000 in your account to cover the potential obligation (100 shares × $310).

| Max Profit | Max Loss | Breakeven |

|---|---|---|

| $500, realized if MSFT remains above $310 at expiration. | $30,500, calculated as $310 (strike price) – $5 (premium) × 100 shares, if MSFT falls to $0. | $305, calculated as $310 – $5. |

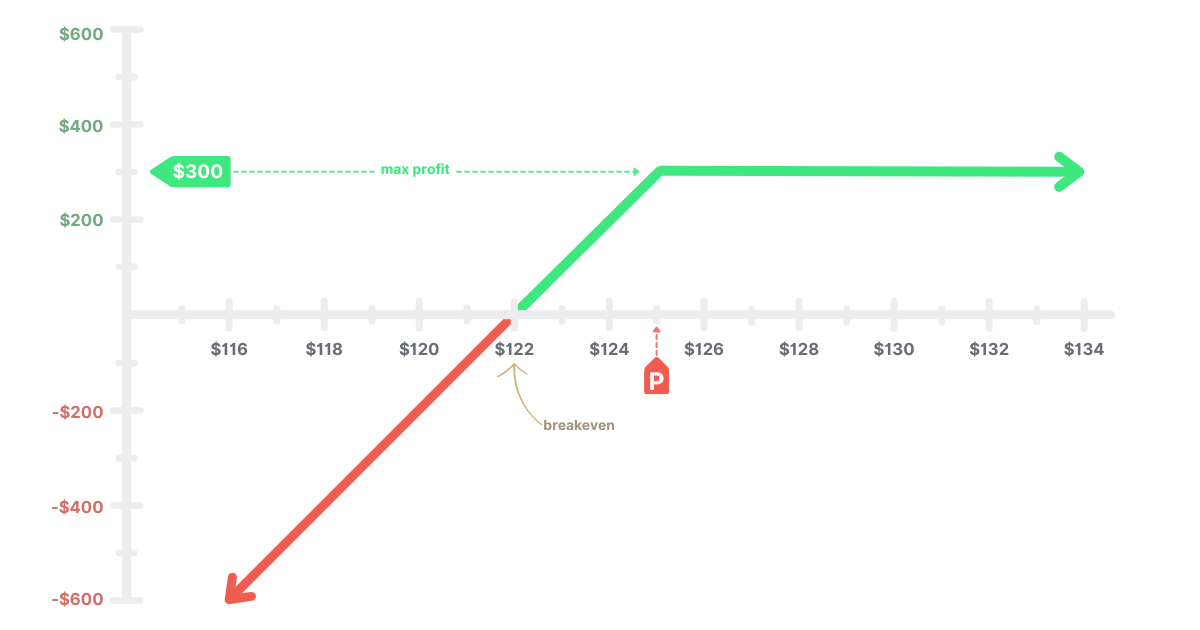

Example 2: Cash-Secured Put on Google

Google (GOOGL) is trading at $130, and you’re interested in owning the stock at a discount:

- Selling the Put: Sell a $125 strike price put and receive a $3 premium per share ($300 total for one contract).

- Cash Requirement: Reserve $12,500 in your account (100 shares × $125).

| Max Profit | Max Loss | Breakeven |

|---|---|---|

| $300, realized if GOOGL stays above $125 at expiration. | $12,200, calculated as $125 (strike price) – $3 (premium) × 100 shares, if GOOGL falls to $0. | $122, calculated as $125 – $3. |

How Option Greeks Influence Your Strategy

The Greeks – Delta, Gamma, Theta, Vega – are like a measuring stick, showing how an option’s price reacts to different market moves. Understanding the greeks can significantly improve your ability to manage and optimize your trades.

Delta (Δ)

Delta measures how much the option price is expected to change for a $1 movement in the underlying stock price. For put sellers, delta is positive, meaning if the stock price goes up, the put’s value decreases (good for you). A lower delta put indicates a lower probability of assignment, making it a safer but less profitable trade.

Gamma (Γ)

Gamma measures the rate at which delta changes as the underlying stock price moves. Higher gamma indicates rapid changes in delta, typically seen as expiration approaches or when the stock price is near the strike price. This means the risk associated with the position can quickly change, requiring closer monitoring as expiration nears.

Theta (Θ)

Theta represents time decay – the rate at which the option loses value each day. Put sellers benefit from positive theta, meaning the value of the option declines daily, helping you earn income over time. Theta increases significantly as expiration approaches, accelerating the rate of profit for put sellers.

Vega (ν)

Vega measures an options sensitivity to changes in volatility. Put sellers have negative vega, benefiting when implied volatility decreases, which reduced the premium. Selling puts when volatility is high allows you to capture larger premiums and potential profits from future declines in volatility.

| Greek | Measures | Put Seller |

|---|---|---|

| Delta (Δ) | Stock price movement | (+) Benefits from stock price increase |

| Gamma (Γ) | Rate of change of delta | (-) Delta decreases as stock price rises and increases as stock price falls |

| Theta (Θ) | Time decay | (+) Benefits from time decay |

| Vega (ν) | Volatility changes | (-) Benefits from volatility decrease |

Why Theta and Volatility Matter

If you’re selling puts, a strong understanding of theta and volatility is essential. These factors directly drive profitability and risk management, shaping the cusses of your cash-secured puts.

Theta (Time Decay)

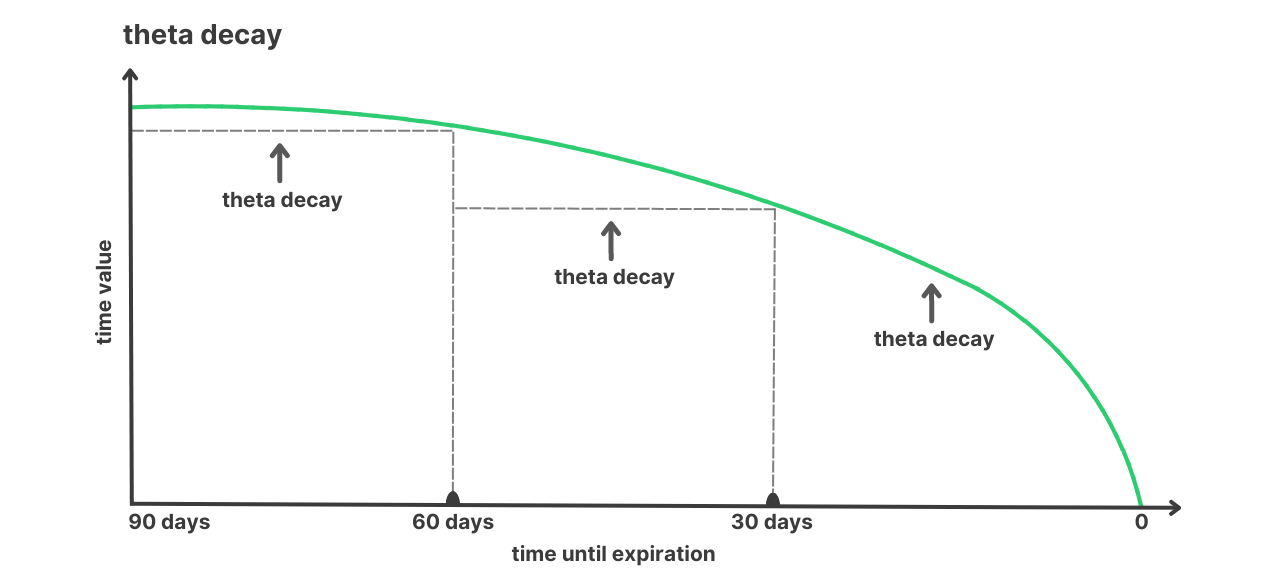

Theta measures the daily decline in an options premium, a key advantage for put sellers. Early in the options life, theta decay is modest, but it accelerates exponentially as expiration approaches, rapidly reducing the premium and boosting profits. For example, a $100 premium might lose $2 daily at 60 days out, but $10 – $15 per day in the final week.

You’ll find traders often sell puts 30-60 days from expiration to capitalize on this increasing decay while retaining flexibility to manage price movements. This timeframe balances higher theta decay with lower gamma risk compared to shorter expirations.

The theta decay curve below illustrates this exponential rise near expiration.

Volatility (Implied Volatility and IV Rank)

Volatility determines the premium you collect when selling the put. Implied volatility (IV) reflects the markets expectation of future stock movement. High IV means more uncertainty, leading to higher option premiums.

This higher volatility is attractive because of the inflated premiums and greater potential profit. Events like earning announcements often spike IV due to this greater uncertainty. After the event this volatility my fall sharply (IV Crush), reducing the premium and allowing sellers to close trades profitably or let the options expire.

To identify options with these inflated premiums, traders may use IV Rank, which compares the current IV to its 12 month range. For example, if the current IV is 30%, with a yearly range of 20% to 40%, the IV Rank is 50%. A high IV Rank signals expensive premium and ideally put vega on your side as the seller.

Managing Your Puts: Closing, Rolling and Accepting Assignment

After you’ve sold your first cash-secured put, you have a few ways to manage it – close, roll, or take the stock.

Closing the Trade

You can choose to close your put early by buying back the option you initially sold. Let’s say you sold a put for $3; if theta decay or a volatility drop (like post-earnings) cuts its value to $0.50, you buy it back and pocket $2.50 per share ($250 per contract). Closing early allows you to capture the profit and reallocate that capital to a new trade.

Rolling the Position

Rolling an option is like hitting reset – you close your current put and sell a new one, often with a later expiration or lower strike. Say your $50 strike put’s nearing expiration, and the stock’s at $51. You buy it back for $1 and sell a 45-day put at $48 for $2, netting more premium and avoiding assignment. By rolling, you extend the trades duration, allowing more time for the underlying stock to potentially recover and often collect additional premium to offset any unrealized losses or reduce your breakeven point.

Accepting Assignment

If the holder of the put chooses to exercise, you as the seller will take assignment and buy the stock at your chosen strike price. This generally occurs at expiration if the stock price is below the strike price of your short put. If you genuinely like the underlying stock and intend to buy it anyway, assignment can be advantageous. You’ll purchase the stock at an effective discount due to the premium received, lowering your overall cost basis and potentially enhancing your long term returns.